If you own residential property in your own name and carry a buy-to-let mortgage, Section 24 has likely increased your tax bill, possibly by thousands of pounds a year.

The rule is straightforward on paper: mortgage interest is no longer deducted from rental income before tax is calculated. Instead you receive a flat 20% tax credit. For basic-rate taxpayers that is broadly neutral. For anyone paying 40% or 45%, it is a permanent and significant increase in tax on the same property with the same income.

This guide covers what Section 24 is, how the calculation works, who it hits hardest, what the real numbers look like, and the five strategies landlords with larger portfolios have used to manage the impact.

1. What Is Section 24?

Section 24 of the Finance (No. 2) Act 2015 removed the right of individual residential landlords to treat mortgage interest as a deductible business expense.

Before this change, if you earned £20,000 in rent and paid £12,000 in mortgage interest, you were taxed on £8,000 of profit. After Section 24, you calculate tax on the full £20,000 and then receive a 20% credit on the £12,000, worth £2,400. The outcome for a higher-rate taxpayer is considerably worse.

The legislation was introduced by George Osborne in the July 2015 Budget, phased in between April 2017 and April 2020, and has been fully in effect since April 2020.

2. What Changed and When

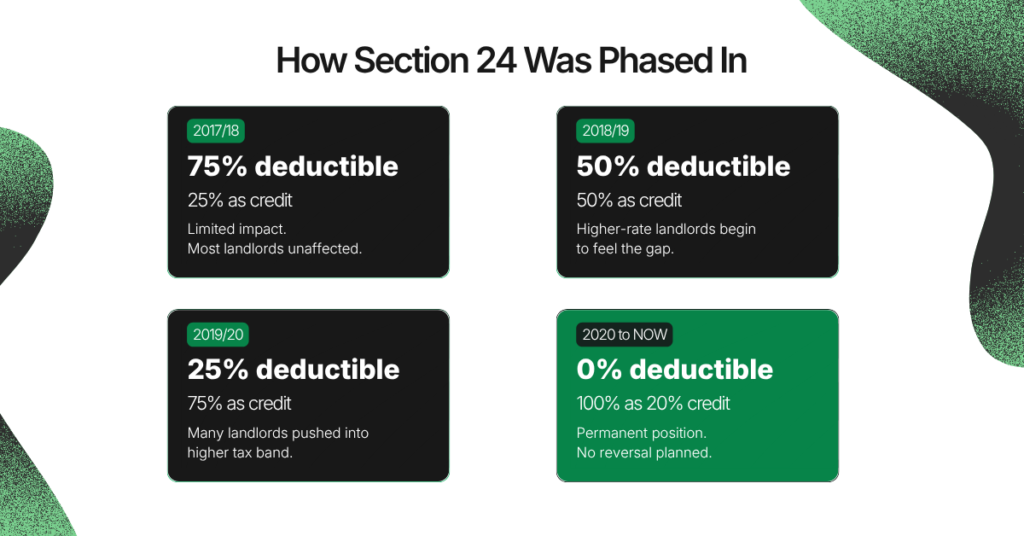

The change was phased in over four tax years to soften the transition. From April 2020 the phase-in was complete and the 20% credit became the permanent position.

2017/18: 75% deductible, 25% as credit

Phase one. Limited impact for most landlords.

2018/19: 50% deductible, 50% as credit

Higher-rate landlords begin to notice the gap widening.

2019/20: 25% deductible, 75% as credit

Many landlords cross into higher tax bands for the first time.

April 2020 onwards: 0% deductible, 100% as credit

Permanent position as of 2026. No reversal planned by either party.

April 2025: Furnished holiday let regime abolished

Announced by Jeremy Hunt in the Spring 2024 Budget, confirmed by Labour in July 2024, and legislated in Finance Act 2025, which enacted the abolition measures announced in the Autumn 2024 Budget. From 6 April 2025, all former furnished holiday let properties are treated identically to standard residential lettings.

April 2026: Making Tax Digital begins (£50,000+ gross income threshold)

Quarterly digital submissions required for landlords above the threshold.

April 2027: Separate property income tax rates announced in the Autumn 2025 Budget

Basic 22% / Higher 42% / Additional 47%. Announced in the November 2025 Budget and included in Finance Bill 2025-26. Verify the current legislative status at bills.parliament.uk and gov.uk before making planning decisions against these figures.

3. Who It Applies To

Section 24 applies to:

- UK residents who let residential property in the UK or overseas

- Non-UK residents who let residential property in the UK

- Individuals who let property as part of a partnership

- Trustees or beneficiaries of a trust paying UK income tax on residential rental income

It does not apply to:

- Limited companies. A company can still deduct mortgage interest in full as a business expense. Corporation tax applies to the net profit. This is the primary reason most new buy-to-let purchases now go through a limited company structure rather than being held in the landlord’s personal name.

- Commercial property landlords. Section 24 covers residential lettings only.

- Furnished holiday let properties (from April 2025). These were exempt under the previous regime. The abolition of the furnished holiday let regime was announced by Jeremy Hunt in the Spring 2024 Budget, confirmed by the incoming Labour government in July 2024, and legislated in Finance Act 2025. From 6 April 2025, all former furnished holiday let properties are treated the same as any standard residential letting and the 20% credit restriction applies in full.

4. How the 20% Tax Credit Works

The mechanics follow five steps. The result can be surprising, particularly for landlords sitting near a tax band threshold.

Step 1: Add up all gross rental income

Total rent received across all personally held residential properties in the tax year.

Step 2: Deduct allowable expenses, not mortgage interest

Repairs, management fees, insurance, accountancy. Mortgage interest is excluded at this stage and does not reduce your taxable profit.

Step 3: Add rental profit to all other income

Salary, pension, dividends, savings interest. This combined total determines your tax band.

Step 4: Calculate income tax on that total

At 20%, 40%, or 45% depending on where your total income falls.

Step 5: Subtract the 20% tax credit

This is 20% of your qualifying finance costs: mortgage interest, arrangement fees, and other loan costs linked to the property. The credit cannot reduce your tax bill below zero and cannot exceed 20% of your gross property profits.

5. Real Numbers: Before and After

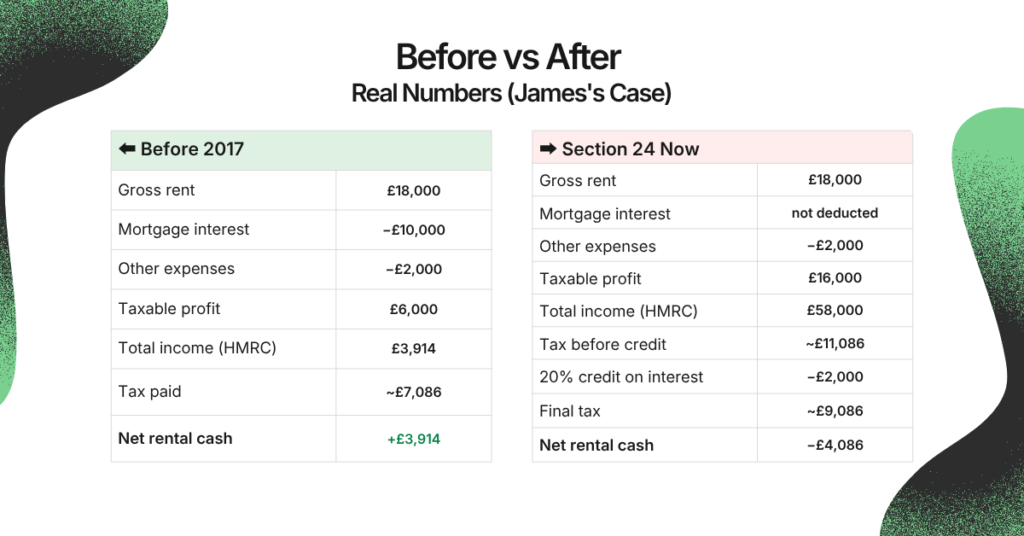

Take a landlord named James. He earns £42,000 from employment and £18,000 gross rent from a buy-to-let property. He pays £10,000 a year in mortgage interest and £2,000 in other allowable expenses.

Under the old rules (pre-2017)

Rental profit: £18,000 minus £10,000 (interest) minus £2,000 (expenses) = £6,000 Total income: £42,000 plus £6,000 = £48,000 (basic rate) Income tax: approximately £7,086 Net rental cash after tax: approximately £3,914

Under Section 24 (current rules)

Taxable rental profit: £18,000 minus £2,000 (expenses only, no interest deduction) = £16,000 Total income (HM Revenue and Customs view): £42,000 plus £16,000 = £58,000 (higher rate) Income tax before credit: approximately £11,086 Minus 20% credit on £10,000 of interest: £2,000 Final income tax: approximately £9,086 Net rental cash after tax and mortgage: a net loss of £4,086

James pays roughly £2,000 more in tax per year. His taxable income is listed by HM Revenue and Customs as £58,000, placing him in the higher-rate band, even though his actual cash position has not changed. He has not earned more. The Section 24 accounting treatment made him appear to.

For a more detailed breakdown of what this costs across a six-property portfolio, including the stacking effect as each property is added, see our guide to Section 24 for portfolio landlords.

6. The Phantom Profit Problem

Because mortgage interest is excluded before calculating rental profit, the taxable income HM Revenue and Customs sees is inflated. This larger number can cross thresholds that trigger additional costs beyond the income tax increase itself. None of these are triggered by actually earning more money.

The higher-rate band at £50,270. A basic-rate landlord whose real cash profit is modest can appear to earn above £50,270 purely due to Section 24. He pays 40% tax on income that produces no extra cash in hand.

The Child Benefit high-income charge above £60,000. The clawback begins at £60,000 of adjusted net income and removes the benefit entirely by £80,000. Phantom rental income can push landlords into this zone without any change to their real earnings.

The personal allowance taper above £100,000. Every £2 above £100,000 removes £1 of personal allowance. At £125,140 the allowance is gone entirely, creating an effective marginal rate of 60% on that slice. A landlord whose real position sits below £100,000 can be pushed above it by Section 24’s treatment of rental income.

Pension annual allowance taper. High earners see their maximum pension annual allowance reduced. This affects landlords who have been using pensions as part of their tax management strategy.

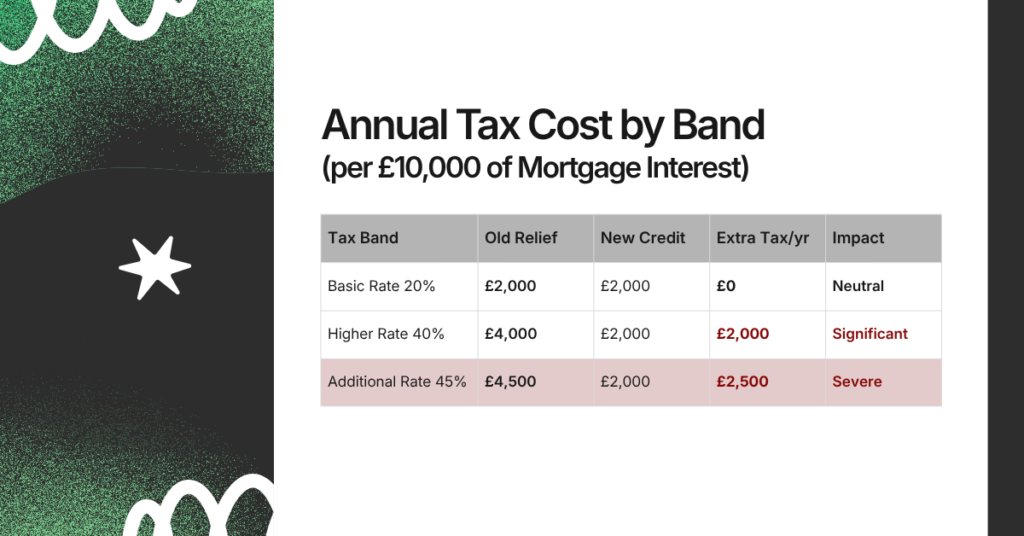

7. Impact by Tax Band

The size of the Section 24 penalty depends entirely on your marginal tax rate. For the current income tax rates and thresholds, verify at GOV.UK.

Basic rate (20%)

Old relief: 20% = £2,000 per £10,000 of interest New relief: 20% = £2,000 Annual gap: £0

Higher rate (40%)

Old relief: 40% = £4,000 per £10,000 of interest New relief: 20% = £2,000 Annual gap: £2,000

Additional rate (45%)

Old relief: 45% = £4,500 per £10,000 of interest New relief: 20% = £2,000 Annual gap: £2,500

For landlords near the higher-rate threshold, the concern is not just the relief gap. It is that Section 24’s phantom profit can push them across the threshold in the first place, turning a neutral situation into a costly one.

8. What You Can Still Deduct in Full

Section 24 only restricts finance costs. All other allowable property expenses remain fully deductible from rental income before tax is calculated. The full list of allowable expenses is set out in the HMRC Property Income Manual.

Fully deductible:

- Letting agent and property management fees

- Landlord insurance premiums

- Repairs and maintenance (like-for-like replacement, not improvements)

- Accountancy fees for rental accounts

- Advertising and tenant-find costs

- Ground rent and service charges on leasehold properties

- Council tax and utilities paid by the landlord during void periods

Restricted to the 20% credit:

- Mortgage interest

- Loan arrangement fees

- Mortgage broker fees

- Interest on loans used to buy, improve, or refinance a residential let

Not deductible at all against income tax:

- Capital repayments on the mortgage principal

- Property improvements and extensions (allowable against Capital Gains Tax on eventual sale, not income tax)

Capital repayments are a common source of confusion. They are not finance costs for Section 24 purposes and cannot form part of the credit. Only the interest portion of a mortgage payment is relevant.

9. Five Strategies Landlords with 3 or More Properties Are Using

There is no single answer. The right strategy depends on portfolio size, current ownership structure, tax position, and how long the properties will be held.

Strategy 1: Incorporate into a limited company

Companies sit outside Section 24. Mortgage interest is fully deductible as a business expense. Corporation tax applies at 19% on profits up to £50,000 and 25% above £250,000.

The obstacle is transferring existing personally held property into a company. HM Revenue and Customs treats this as a sale at market value, triggering Stamp Duty Land Tax (including the 5% additional dwellings surcharge, in force from 31 October 2024) and potentially Capital Gains Tax on any accumulated gain. For a portfolio worth £500,000, those transfer costs can be substantial.

From April 2026, Incorporation Relief under Section 162 TCGA 1992 must be actively claimed. It is no longer automatic. The property activity also needs to meet the threshold of constituting a genuine business, which requires professional assessment.

Incorporation works best for landlords with larger portfolios, long remaining hold periods, and higher-rate tax positions where the annual saving eventually outweighs the one-off transfer costs.

Strategy 2: Pay down the mortgage

Less mortgage debt means less interest, which means a smaller Section 24 liability. For landlords with surplus cash, overpaying a buy-to-let mortgage often delivers a better after-tax return than savings accounts or other low-risk alternatives.

The trade-off is capital tied up in property and reduced liquidity. But as a way to reduce taxable phantom income, it works.

Strategy 3: Transfer beneficial interest to a lower-earning spouse or civil partner

If one partner is a basic-rate taxpayer and the other pays higher-rate, restructuring ownership can shift rental income toward the lower tax band.

This requires severing the joint tenancy to become tenants in common, agreeing and documenting the ownership split, and filing Form 17 with HM Revenue and Customs within 60 days. It must reflect genuine legal ownership. HM Revenue and Customs scrutinises these arrangements closely.

Strategy 4: Increase pension contributions

Pension contributions reduce adjusted net income, which HM Revenue and Customs uses to assess tax band thresholds, Child Benefit charges, and personal allowance tapers. A landlord sitting just above £60,000 or £100,000 could bring phantom Section 24 income back below key thresholds through employer or personal pension contributions.

This does not remove the Section 24 restriction itself but can reduce the knock-on effects significantly.

Strategy 5: Sell and redeploy

For properties with high loan-to-value ratios, modest yields, or unfavourable long-term prospects, the honest calculation sometimes shows that selling makes more financial sense than continuing to hold.

Some landlords have used sale proceeds to invest in structures that avoid the restriction entirely, including limited company buy-to-let or commercial property.

10. Making Tax Digital: What Changes from April 2026

Making Tax Digital for Income Tax replaces the annual self-assessment return with quarterly digital submissions through HM Revenue and Customs-recognised software. The rollout is phased by gross income threshold.

6 April 2026: Landlords with gross rental or self-employment income over £50,000 in the 2024/25 tax year.

6 April 2027: The threshold drops to £30,000 (based on 2025/26 income).

6 April 2028: The threshold drops further to £20,000 (based on 2026/27 income).

The thresholds apply to gross rental income before any expenses are deducted, not net profit. If you own three or more properties generating £1,000 or more per month each, your gross income is likely above £36,000 and you are probably caught by the April 2027 threshold even if you fall below April 2026. Joint owners each count their individual share separately toward their own threshold.

Under Making Tax Digital, landlords submit four quarterly updates per year summarising income and expenses, then file a final declaration by 31 January. All submissions must come through HM Revenue and Customs-recognised compatible software. A spreadsheet or paper records will no longer be sufficient once your threshold is reached.

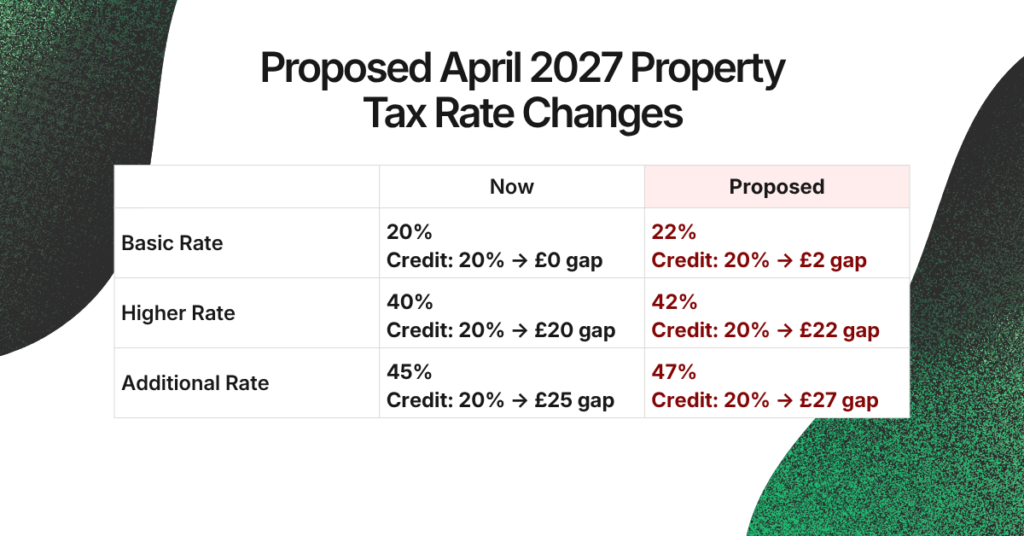

11. April 2027: Announced in the Autumn 2025 Budget (Verify Before Acting)

Separate income tax rates for property income were announced in the November 2025 Autumn Budget and are included in Finance Bill 2025-26. Verify the current status of this legislation at bills.parliament.uk and gov.uk/income-tax-rates before making planning decisions against these figures.

The 20% tax credit under Section 24 is expected to remain at 20%. As the rates rise, the gap between what landlords pay on rental income and what they recover through the credit would widen further.

- Basic rate: currently 20%, proposed to rise to 22% from April 2027 (2 point gap vs 20% credit)

- Higher rate: currently 40%, proposed to rise to 42% from April 2027 (22 point gap vs 20% credit)

- Additional rate: currently 45%, proposed to rise to 47% from April 2027 (27 point gap vs 20% credit)

For a higher-rate landlord with £10,000 of annual mortgage interest, the current Section 24 cost is £2,000 per year. If the April 2027 rates are legislated as announced, that would rise to £2,200 on the same property with no change to income or borrowing. For additional-rate landlords the same £10,000 of interest would rise from £2,500 to £2,700 annually.

The finance restriction has been permanent since 2020. Speak with a qualified adviser to understand what the proposed rate changes would mean for your specific position.

Frequently Asked Questions

Does Section 24 apply if I only own one property?Yes. It applies to all individual landlords of residential property in the UK regardless of portfolio size. One property or twenty, if it is held in your own name and carries a mortgage, the restriction applies.

Can I still claim mortgage interest as a landlord?Yes, but not as a direct deduction from rental income. You claim a 20% tax credit on qualifying finance costs after calculating your taxable profit. The credit reduces your income tax bill rather than reducing the profit the tax is calculated on. For a full explanation of how rental income is taxed in the UK, see our dedicated guide on the topic.

Does Section 24 apply to limited companies?No. Companies can still deduct mortgage interest in full against rental income. Corporation tax is paid on the net profit. This is the main reason most new buy-to-let purchases now go through a limited company structure rather than being held in the landlord's personal name.

What counts as finance costs for the 20% credit?Mortgage interest, loan arrangement fees, mortgage broker fees, and interest on any loan used to buy, improve, or refinance a residential let. Capital repayments do not qualify. Only the interest portion of your mortgage payment is relevant.

I am a basic-rate taxpayer. Does Section 24 affect me?Possibly. If your total income, including the inflated taxable profit Section 24 creates, stays below the £50,270 higher-rate threshold, the impact is broadly neutral. But the phantom profit effect can push basic-rate landlords across that line without any actual increase in income.

Where do I enter finance costs on my self-assessment?Residential finance costs go in Box 44 of the UK Property pages (form SA105) of your self-assessment return. Box 45 is for any unused residential property finance costs brought forward from earlier years. Box 26, which was historically used for furnished holiday let finance costs, is now defunct following the abolition of the furnished holiday let regime from 6 April 2025.

Does Section 24 apply to furnished holiday let properties? Yes, since 6 April 2025. The abolition of the furnished holiday let regime was announced by Jeremy Hunt in the Spring 2024 Budget, confirmed by Labour in July 2024, and legislated in Finance Act 2025. All individually owned residential rental properties, including former furnished holiday lets, are now subject to the 20% credit restriction. See our guide to holiday let tax breaks still available in 2026 for what remains claimable.

Are the April 2027 property tax rate increases definitely happening? They were announced in the November 2025 Autumn Budget and are included in Finance Bill 2025-26. Verify the current legislative status at bills.parliament.uk before relying on these figures for planning purposes. The basic rate of income tax on property income is proposed to rise to 22%, the higher rate to 42%, and the additional rate to 47%, all from 6 April 2027. The 20% credit under Section 24 is expected to remain unchanged.

Published May 2026. Last reviewed May 2026. For information only and not tax advice. Verify current figures at GOV.UK. Speak with a qualified adviser for guidance on your specific circumstances.